There are several simple Financial Rules that can help a common person make better financial decisions in daily life. Being in good financial health means that you can cover expenses and save for the times ahead. These financial thumb rules can be used by those who are just beginning their financial journey as well as others who are already on their path. There’s no ‘one size fits all’ funda and these financial rules only provide you with a basic understanding.

From this article, you’ll discover how to determine your financial wellness level and what financial rules to follow to improve your financial health.

- Building a strong financial foundation starts with smart budgeting and disciplined saving. By following proven financial rules, you can create a balanced approach to managing expenses, growing your savings, and securing your financial future.

50/30/20 Budgeting Rule: The Smart Way to Manage Your Money

Managing personal finances can feel overwhelming, but the 50/30/20 budgeting rule simplifies the process. By allocating 50% of income to needs, 30% to wants, and 20% to savings, this method creates a structured yet flexible financial plan.

The 50/30/20 rule was popularized by U.S. Senator Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan.” It is a straightforward method to ensure that you cover essentials, enjoy life, and save for the future without overcomplicating money management.

It helps in managing income for expenses, savings, and investments.

This 50/30/20 Budgeting Rule says that you should break down your income in three parts.

- 50% for needs Essential expenses such as rent, groceries, transportation, healthcare, and loan payments.

- 30% for wants non essential expenses like entertainment, dining out, travel, and shopping.

- 20% for emergency funds, savings, debt repayment, and investments.

Example

If you earn ₹50,000 per month:

| Category | Percentage | Amount (₹) | Examples |

| Needs | 50% | 25,000 | Rent, utilities, groceries, loan payments |

| Wants | 30% | 15,000 | Dining out, entertainment, shopping, travel |

| Savings | 20% | 10,000 | Savings, Emergency fund, investments |

If you live in an expensive city like Ahmedabad or Mumbai, high rent might eat up more than half of your income. When that happens, you either cut back on non essentials or adjust your savings to maintain balance. If you earn a high salary, saving more than 20% can help you build wealth faster.

The 50/30/20 budgeting rule makes managing money simple. You can easily follow it, adjust your spending (especially in the “wants” category), and find the right balance between enjoying life now and securing your future.

Keep in mind that this financial rule applies to your net income the money you actually take home after taxes and deductions.

By tracking your expenses and making changes, when necessary, you stay in control of your finances while still enjoying life. The 50/30/20 rule gives you a simple but flexible plan, helping you save for the future while still enjoying what’s important to you.

- Managing debt wisely is essential for maintaining financial stability and avoiding unnecessary stress. By following key debt management principles, you can borrow responsibly, keep payments manageable, and work toward a debt-free future.

35% Debt Rule: The Secret to Smart Debt Management

The “35% Debt Rule” is a guideline that focuses on managing your overall debt burden, particularly when it comes to loans and Equated Monthly Instalments (EMIs). Helps ensure loans/EMIs are within control.

- Financial Rule: Total EMIs should not exceed 35% of monthly income.

For an example If you earn ₹80,000 per month, total EMIs (home, car, personal loan) should be ≤ ₹28,000.

How 35% Debt Rule Works?

At first Calculate your total monthly debt payments (e.g., credit card payments, personal loans, car loans, home loans, etc.). After that calculate your gross monthly income (your income before taxes and other deductions). Divide your total monthly debt payments by your gross monthly income. Multiply the result by 100 to get the percentage. Aim to keep this percentage below 35%.

The “35% Debt Rule” (also known as the debt to income or DTI ratio) suggests that your total monthly debt payments, including home loan EMIs and other loans, should ideally be 35% or less of your gross monthly income to ensure financial stability. This is a straightforward and simple financial rule. This financial rule is used to prevent excessive debt accumulation and ensure that you have enough income left for other essential expenses and savings. This easy financial rule helps in managing personal financial debt. Also, it helps maintain a good credit score. It ensures financial flexibility for savings and investments.

10% Savings Rule: The Key to Long Term Wealth

The “10% Savings Rule” is a simple and widely recommended guideline for personal finance. The basic idea is to consistently set aside a portion of your earnings for future financial goals. Essentially it helps develop a habit of saving money.

The 10% savings rule suggests saving a minimum of 10% of your income, whether it’s gross or post-tax income, to build a financial cushion and achieve your goals. While 10% is a good starting point, you can gradually increase your savings as your income grows. Some budgeting models like the 50/30/20 rule or 40/30/20/10 rule also helps savings as a percentage of income.

- Rule: Save at least 10% of your income every month before spending.

For example, if you earn ₹60,000 per month, save at least ₹6,000.

Whole logic of this 10% rule is the emphasis on regular savings, even if the amount is relatively small.

It should be noted that although 10% is the general guideline, you can adjust the percentage based on your individual circumstances and financial goals and many financial experts recommend saving significantly more than 10% if it is possible and sustainable.

It’s an easy to understand and implement financial rule, making it accessible to people at all financial levels. 10% Savings Rule contributes to building a financial safety net and achieving long term financial goals. It helps as small and consistent savings grows significantly over time due to compounding.

It should be considered that while the 10% Savings Rule is a good starting point, it may not be sufficient for everyone. One should consider individual circumstances, such as income level, expenses, and financial goals, when determining savings rate. It is often easier to save money if the saving is automated. Have a set amount of money automatically transferred from your salary account to your savings account on a regular basis.

Summarily, the 10% Savings Rule encourages a proactive approach to saving, laying the foundation for financial wellbeing.

The Emergency Fund Rule: How Much Should You Really Save?

An emergency fund is the money which are kept aside for use during time of unexpected requirement of money during financial emergencies like hospital bill, job loss or any such needs.

A common rule of thumb for emergency funds is to save three to six months of living expenses.

- Rule: Save 3 to 6 months of monthly expenses in a liquid fund essential living expense.

For Example, if your monthly expenses are ₹40,000, your emergency fund should be ₹1.2 lakh to ₹2.4 lakh.

How to build an emergency fund?

Set a clear savings goal for each month knowing exactly what you’re aiming for makes all the difference. As soon as your salary gets credited, move a portion straight into your savings account before you get the urge to spend. Seriously, treat it like a bill you have to pay. The trick? Automate the transfer if possible, so saving becomes effortless.

Where to keep your emergency fund?

Money in Your emergency fund should be easily accessible. A high interest savings account is a good option since it keeps your money safe while earning interest.

The amount you need depends on your lifestyle, income, housing costs, utilities, groceries, transportation, healthcare, and debt payments. If you have a stable job and no dependents, a smaller fund may be enough. If you have dependents, you’ll need more.

Use your emergency fund only for urgent, unexpected expenses. If you withdraw from it, replenish it quickly. Prioritize building this fund before aggressively paying off debt or investing.

Why emergency fund is important?

Building an emergency fund is a smart way to prepare for life’s uncertainties and stay financially stable.

An emergency fund gives you financial security and peace of mind. It prevents you from falling into debt or relying on high-interest loans during emergencies. With a safety net in place, you can handle unexpected expenses without disrupting your long-term financial goals.

- Growing your wealth isn’t just about saving, it’s about making your money work for you. Understanding key investment and inflation principles can help you maximize returns, preserve purchasing power, and build long-term financial security.

7% Inflation Rule: Understanding the Impact of Inflation

This is a simple rule of thumb used to estimate how long it takes for an investment to double or for the purchasing power of money to halve, based on a given annual interest rate or inflation rate.

The “7% Inflation Rule” uses the financial rule of 72 to estimate that with a 7% annual inflation rate, the purchasing power of money halves in approximately 10 years (72 / 7 = 10).

Inflation reduces the value of money over time, meaning that the same amount of money will buy fewer goods and services in the future.

- Rule: If inflation is 7%, the value of money halves in 10 years (using Rule of 72: 72 ÷ 7 = 10).

If you have ₹1000 today, with a 7% inflation rate, in 10 years that ₹1000 will have roughly half the purchasing power, meaning you’d need ₹2000 to buy the same goods and services. If rent is ₹10,000 per month today, in 10 years, it might be around ₹20,000 assuming steady 7% inflation.

Look at real world examples of inflation’s Impact in India, in 1995, ₹10 could buy a full meal at a roadside eatery. Today, the same meal costs around ₹100 or more, showing how inflation reduces purchasing power. One should keep in mind that while this 7% Inflation Rule is simple and easy, it assumes constant inflation, whereas real life inflation fluctuates.

1% Increase Rule: Small Steps to Big Financial Growth

The 1% Increase Rule is a simple yet effective strategy for gradually boosting savings without feeling a significant financial strain. The 1% Increase Rule suggests a gradual approach to improving savings by increasing your savings rate by 1% annually, starting from your current level.

The primary goal of this financial rule is to make saving more manageable and sustainable by avoiding large, potentially overwhelming changes in your budget.

- Rule: Increase savings rate by 1% every year.

For example, if you are saving 10% of income in current year, then by increase 1% next year. If you continue this practice at 10th year you would be saving 20% of your income.

By consistently allocating a portion of your income to savings, you become more financially aware and understand the importance of saving for the future.

The gradual approach makes it easier to adjust your spending habits and build a comfortable savings buffer without feeling overly restricted.

Over time, consistent savings, even in small increments, can lead to significant financial security and help you achieve your long-term goals.

4% Withdrawal Rule: A Guide to Retirement Planning

The 4% withdrawal rule helps retirees estimate how much they can withdraw annually from their savings without running out of their funds.

- Rule: Withdraw 4% of total retirement savings per year.

If you have ₹1 crore saved, you can withdraw ₹4 lakh per year (adjusted for inflation).

Bill Bengen, a financial adviser in Southern California created this financial rule around mid 1990s. He developed this rule using historical stock and bond return data from 1926 to 1976. He analysed financial crises like the Great Depression and the early 1970s recession to find a withdrawal rate that could sustain a retiree’s savings through various market conditions.

This financial rule is simple to follow and provides predictable, steady income for future years. Many financial experts debate whether 4% is the best withdrawal rate. Even Bill Bengen, the financial advisor who introduced this financial rule in the 1990s, suggested that 5% might work better, except during extreme economic downturns.

The 4% withdrawal rule is a decent rule of thumb for retirement planning. But let’s be real, it’s not a one size fits all solution. Your financial future depends on way more than a simple percentage. Market ups and downs, your unique spending habits, and how you invest, all play a huge role. Instead of blindly sticking to a formula, it’s smarter to sit down with a financial expert who can help craft a withdrawal plan that actually works for your lifestyle.

The Rule of 72: The Simple Financial Rule to Double Your Money

This ‘Rule of 72’ gives you an estimate of the number of years it will take to double your money in a particular investment tool. The rule of 72, which was derived before the 14th century, is still a quick, mental calculation for the effects of compound interest.

The “Rule of 72” is a method of estimating how long it will take compounding interest to double an investment. Just divide 72 by interest rate, and get number of years to get your money double.

- Formula: 72 / [Annual interest rate] = [number of years to double principal]

For an example at 8% annual return, money doubles in 9 years (72 ÷ 8).

If the rate of interest is 9%, simply divide the number 72 by 9% and the answer is 8. Thus, it will take 8 years to double your money if you invest at 9% p.a. rate of interest.

One interesting fact that we can use this financial rule in reverse to know the rate of interest needed to double your money to achieve your set goal. If you have ₹2,50,000 today and need ₹5,00,000 in 5 years, you can use the ‘rule of 72’ to estimate the required annual rate of return. By dividing 72 by 5, you find that you need approximately a 14.4% annual return. Therefore, you should seek investment options that offer at least a 14.4% annual rate of return to double your investment in 5 years.

Things to keep in mind for this financial rule

This ‘Rule 72’ helps you to understand about inflation also. It helps you to calculate the amount of time it will take for inflation to make the real value of money half. Let’s say the present inflation is 5.5%. When you divide 72 by 5.5% the answer is 13.09 years. That is to say, if you have 100k in your kitty today, it would take around 13.09 years for the value of the money to be halved.

Inflation reduces purchasing power over time, and the Rule of 72 can help estimate how long it will take for inflation to cut the real value of money in half.

If you have a set financial goal and a time frame, you can use the Rule of 72 in reverse to determine the required interest rate.

The Rule of 72 helps you quickly estimate how long it takes for an investment to double. Just divide 72 by the interest rate, and you’ll get a rough idea of how many years it will take. No complex formulas or calculators, just quick math!

But like any shortcut, it has limits. Its accuracy drops with very high or very low interest rates. It works best when rates stay between 5% and 15% outside that range, the estimate becomes less reliable.

The rule also assumes a fixed interest rate, but in reality, rates often fluctuate, especially in the stock market. And if you’re dealing with simple interest instead of compound interest, this financial rule won’t give you an accurate result.

Still, the Rule of 72 makes financial decisions easier. It helps you estimate investment growth, inflation impact, and the power of compounding. Whether you’re an investor, a business owner, or someone planning for the future, this simple formula can guide your choices.

Use it as a quick mental shortcut, but keep its limitations in mind. While it’s not a perfect formula, it remains one of the most useful finance tricks ever discovered. Hope it helps you in your day to day investments and other financial activities.

Rule of 114: The Tripling Rule for Investment Growth

The “Rule of 114,” or the tripling rule, is a simple method to estimate the time it takes for an investment to triple, by dividing 114 by the expected annual rate of return.

Rule of 114: To estimate when your money will triple, divide 114 by the annual interest rate.

For an 8 percent return, 114/8 = 14.25 years. Thus, your money will triple in about 14.25 years.

A quick and easy way to estimate how long it takes for your money to triple at a given annual return rate.

Use: Estimate how long an investment takes to triple at a fixed return rate.

Divide 114 by the annual return rate (as a percentage) to get the approximate number of years it will take for your investment to triple.

- Formula: Tripling Time = 114 / Annual Return Rate (%)

Example: At 10% interest, money triples in 11.4 years (114 ÷ 10). At a 12% annual return, the tripling time would be approximately 114 / 12 = 9.5 years.

This rule is considered ideal for investors of all experience. This financial rule offers a rough amount for tripling the investment. Rule 114 provides a reasonable timeframe than anticipating an overnight double in the money. It’s a quick way to gauge the potential impact of compounding over time. It is often spoken of in conjunction with the rule of 72, which calculates the time required for an investment to double.

Rule of 144: The Quadrupling Rule for Wealth Creation

This nifty little rule helps estimate how many years it will take for an investment to quadruple (yes, 4x!) in value, assuming you’re earning compound interest. The beauty of compound interest? It’s basically your money making more money, and then that extra money making even more!

Formula: Years to Quadruple = 144 / Annual Return Rate (%)

At 12% interest, money quadruples in 12 years (144 ÷ 12). For instance, if you anticipate an annual return of 8%, your investment would approximately quadruple in 18 years (144 / 8 = 18).

It’s a quick and easy way to estimate how long it will take for your money to quadruple, making it an essential tool for anyone planning their financial future.

By knowing how long it might take for your money to grow 4x, you can make more informed decisions about where to invest and how long to stay invested.

The Rule of 144 works best for investments that benefit from compound interest, meaning your earnings keep generating more earnings over time. The longer you stay in the game, the more powerful compounding becomes.

20/4/10 Car Buying Rule: Making Smart Auto Purchases

The 20/4/10 rule is a financial rules (guideline) designed to help individuals make wise car buying decisions without straining their budget.

- Rule:

- Pay at least 20% as down payment.

- Take a loan for not more than 4 years.

- EMI should not exceed 10% of monthly income.

For example, if you earn ₹70,000 per month, your EMI should not exceed ₹7,000.

20% Down Payment

The rule advises a down payment of at least 20% of the car’s price. This reduces the loan amount, lowering monthly payments and total interest. It also builds immediate equity, which helps if the car depreciates quickly.

4 Year Loan Term

The rule recommends financing the car for no more than four years (48 months). Shorter loan terms typically have lower interest rates, reducing overall costs. They also help prevent the loan balance from exceeding the car’s value as it depreciates.

10% of Monthly Income

The rule advises keeping all car-related expenses loan payments, insurance, maintenance, and fuel within 10% of your gross monthly income. This helps keep transportation costs manageable, leaving room for other essential expenses and savings.

20/4/10 Car Buying Rule encourages saving a substantial down payment to lower the car’s total cost and reduce monthly payments. A short loan term helps buyers pay off the car faster and minimize interest charges. Keeping monthly car expenses in check ensures financial stability, making it easier to manage other responsibilities.

Enables smart car purchases while maintaining financial stability. Encourages considering all expenses to prioritize financial well-being. Ideal for those who distinguish needs from wants and align choices with financial goals. Guides first-time buyers in making practical, budget-friendly decisions.

3X Salary Rule for Buying a Car: Can You Afford It?

The “3X Salary Rule” for car buying suggests that you should aim to spend no more than three times your monthly salary on a car to avoid overspending and ensure financial stability.

This financial rule ensures you don’t overspend on a car. It helps you determine a reasonable budget for a car purchase, preventing you from taking on excessive debt.

- Rule: Buy a car that costs no more than 3 times your monthly salary.

For example,if your monthly salary is ₹50,000, your car’s price should not exceed ₹1.5 lakh. In the Indian context, the 20/4/10 car buying rule (20% down payment, 4-year loan, and 10% of income for car expenses) is generally considered more practical than the 3X salary rule, as it offers a more balanced approach to car financing and budgeting.

5X Salary Rule for Buying a House: A Realistic Approach

The “5X Salary Rule” suggests that the cost of your home should ideally not exceed five times your annual salary, helping you determine a reasonable home loan amount and budget. It helps determine how much home loan you should take.

- Rule: Your home cost should not exceed 5 times your annual salary.

For example, if your annual salary is ₹10 lakh, your home should cost ≤ ₹50 lakh.

The 5X Salary Rule is a helpful guideline, but it’s not a one size fits all solution. Your financial situation, savings, and long term goals should also influence your home buying decision. Always plan wisely and consult a financial advisor if needed before making a big purchase like a home. This financial rule helps you avoid financial strain when buying a house and guides you in choosing a manageable home loan. By sticking to this rule, you can ensure that your monthly mortgage payments (including principal, interest, property taxes, and insurance) don’t strain your budget and allow you to save and invest for other financial goals.

- Small, everyday expenses can quietly drain your finances without you even realizing it. By being mindful of spending habits and making intentional choices, you can free up more money for savings, investments, and future goals.

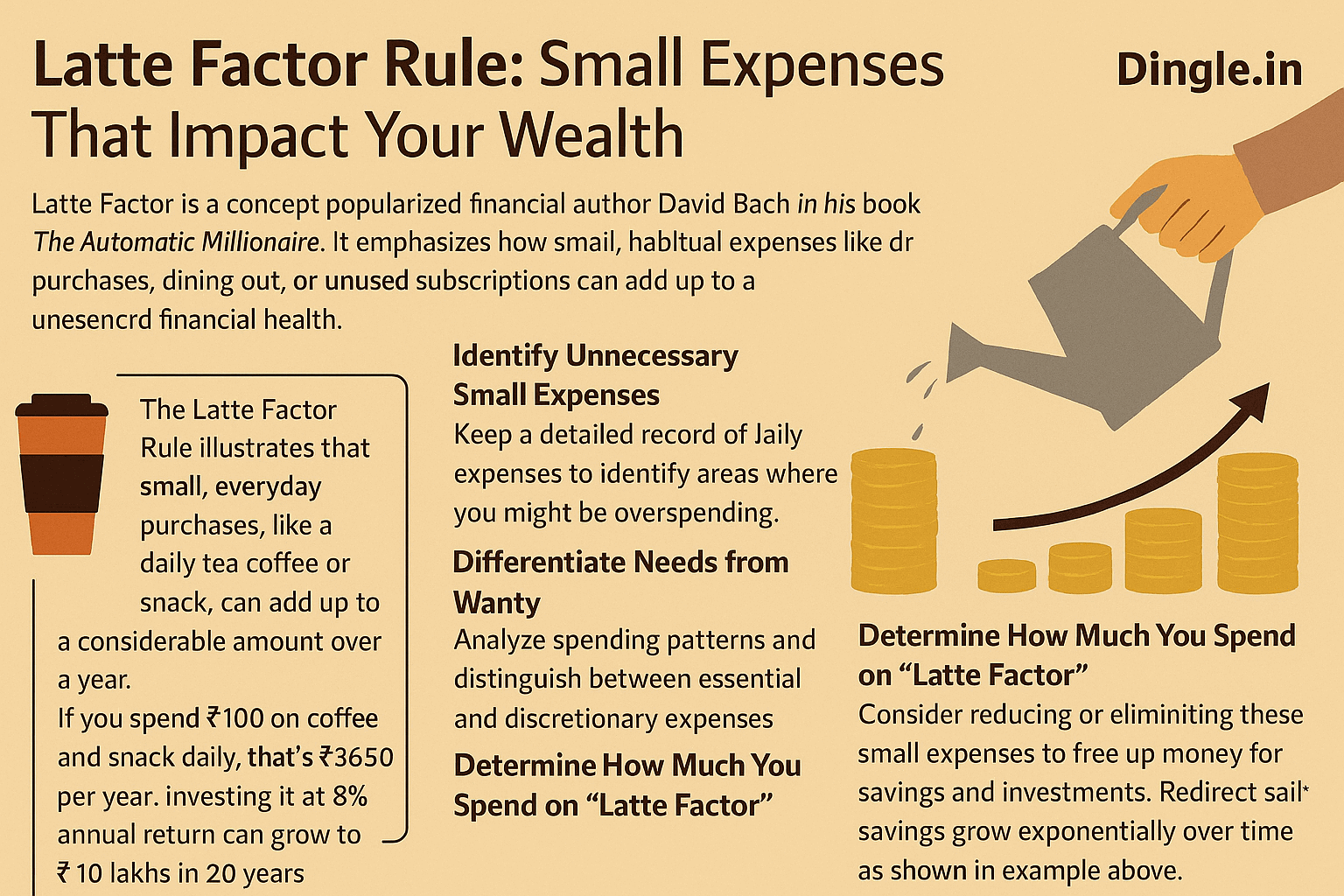

Latte Factor Rule: Small Expenses That Impact Your Wealth

The Latte Factor is a concept popularized by financial author David Bach in his book The Automatic Millionaire. It emphasizes how small, habitual expenses like daily coffee shop purchases, dining out, or unused subscriptions can add up over time and significantly impact financial health.

- The Latte Factor Rule illustrates that small, everyday purchases, like a daily tea coffee or snack, can add up to a considerable amount over a year.

Example: If you spend ₹100 on coffee and snack daily, that’s ₹36,500 per year. Investing it at 8% annual return can grow to ₹10 lakhs in 20 years.

This concept suggests one to identify unnecessary small expenses. For this one should keep a detailed record of daily expenses to identify areas where you might be overspending.

After that differentiate needs from wants. Analyse spending patterns and distinguish between essential and discretionary expenses.

Determine how much you spend on “Latte Factor” or Non Essential items daily, weekly, monthly, and yearly. At last, consider reducing or eliminating these small expenses to free up money for savings and investments. Redirect savings into investments or savings accounts. These small savings grow exponentially over time as shown in example above.

The Latte Factor doesn’t just mean cutting tea or coffee. Instead, spend mindfully. If tea or coffee brings you joy, then trim other small expenses or make your spending align with your priorities.

Conclusion: Simple Financial Rules for a Better Future

Following these financial rules can make managing money easier and help you build a secure future. Whether it’s budgeting wisely with the 50/30/20 rule, saving 10% of your income, or using the financial Rule of 72 to grow your investments, these guidelines can lead to financial success. Small steps, like cutting unnecessary expenses and saving a little more each month, can make a big difference over time. The key is to stay consistent and make smart money choices.

Start applying these financial rules today, and you’ll be on your way to a stress free financial future!

Take care.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.